It’s often said the only free lunch in investing is diversification; placing investments across different asset classes, industries and geographies. Most investors do a pretty good job of the first two but tend to fall short when it comes to the ‘geography’ part.

Be it in Australia or overseas, a ‘home bias’ emerges where investors overwhelmingly favour companies in the country they live, ignoring the rest of the world. And it’s not hard to understand why; these markets are easier for domestic investors to access, the companies are more familiar, and the prevalence of specialised local asset management firms means they tend to be front-of-mind.

The risk of concentration

The problem with owning stocks in just one country or a limited number of countries is that portfolios become concentrated and therefore vulnerable to the same events – currency movements, interest rates, political upheaval, weather events, recessions – and vulnerable to the significant loss of capital.

Spreading assets across different regions ie. diversifying, can help insulate portfolios from concentration risk.

2020 illustrated the opportunity cost is real

While global equities markets can move in tandem, there can also be notable differences in performance – while one geographic region may be performing poorly, another may be performing strongly.

Variation in performance exists as specific markets are driven by specific factors. Last year was a case in point.

In 2020 the performance of the major US indices varied dramatically, with the Nasdaq Index returning 45%, compared to the S&P500 Index +18% and the Dow Jones Industrial Average Index +10%.

The Nasdaq contained companies with a much greater exposure to the tech titans, who were (and still are) beneficiaries of the COVID-19 lockdowns.

Over the same period, the average returns of China’s onshore equities stood at almost 30%1. The Chinext Composite Index, a Nasdaq-style exchange board seeking to attract innovative and fast-growing enterprises, particularly high-tech firms, increased by almost 45%.

Comparatively, the Australian stock market returned investors +1.4%.

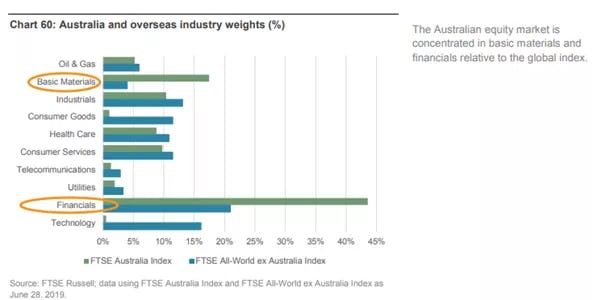

More broadly, Australian investors have been short changed when it comes to sector diversification benefits. The two most prominent sectors in the ASX200 Index account for almost 50% of the Index; Financials (29%) and Base Materials (21%). The index is significantly underweight Technology stocks which makes up just 5% of the Index compared to 27% in the S&P500.

As recognised by Brian Arthur, the Santa Fe Institute’s theoretical economist in his ground breaking paper almost a quarter century ago, ‘Increasing Returns and the New World of Business’, traditional industries tend to be subject to diminishing returns while technology companies can be subject to increasing returns; they grow stronger and more profitable as they evolve.

What the above illustrates is the real opportunity cost for those investors – and in particular Australian investors in 2020 – with a home bias and geographically concentrated portfolios.

Australia’s home bias inhibits investment returns

Australian investors could have countered this lack of diversification by investing offshore.

Research by the Financial Times Stock Exchange Group (FTSE) shows Australia’s home bias is the largest of the major pension markets, and by a significant margin, with the average allocation to overseas equities at just 47%.

This statistic is particularly striking when you consider Australia constitutes less than 2% of the FTSE All-World Index, implying a home bias ratio of 26 times2. This is much higher than home-bias ratios in other developed markets such as the US at 1.2 times, Japan at 4.3 times and the UK at six times.

The FTSE paper concluded Australia’s home-bias had been an inhibitor of investment returns. Australian investors are foregoing opportunities in many of the world’s best companies in emerging industries in some of some of the fastest growing regions in the world.

Why geographic diversification can be a lifesaver

A 2019 research paper by asset manager Bridgewater Associates titled ‘Geographic Diversification Can Be A Lifesaver – Yet Most Portfolios Are Highly Concentrated’, highlights the wealth preservation and return benefits from adding different geographic exposures to a portfolio.

“One common vulnerability is geographic concentration. In the past century, there have been many times when investors concentrated in one country saw their wealth wiped out by geopolitical upheavals, debt crises, monetary reforms, or the bursting of bubbles, while markets in other countries remained resilient.

Even without such extreme events, there is always a big divergence across the best and worst performing countries in any given period. And no one country consistently outperforms, as outperformance can lead to relative overvaluation and a subsequent reversal.

Rather than try to predict who the winner will be in any particular period, a geographically diversified portfolio creates a more consistent return stream that tends to do almost as well as whatever the best single country turns out to be at any point in time.

So geographic diversification has big upside and little downside for investors.”

- Bridgewater Associates

Investors have overlooked China – to date

In recent years, there has been an increasing recognition of the benefits of adding China equities exposure to a global portfolio. China’s emergence as an economic super-power, its transition to a more sustainable consumption and innovation-led services model, and its low historic correlation to other asset classes have started to attract the attention of global investors.

Bridgewater’s aforementioned research paper noted:

“China’s ascent as an important economic and financial centre with divergent secular conditions from much of the developed world (e.g. more ability to stimulate in the event of a downturn) raises the likelihood of an increasingly multipolar and less correlated world.

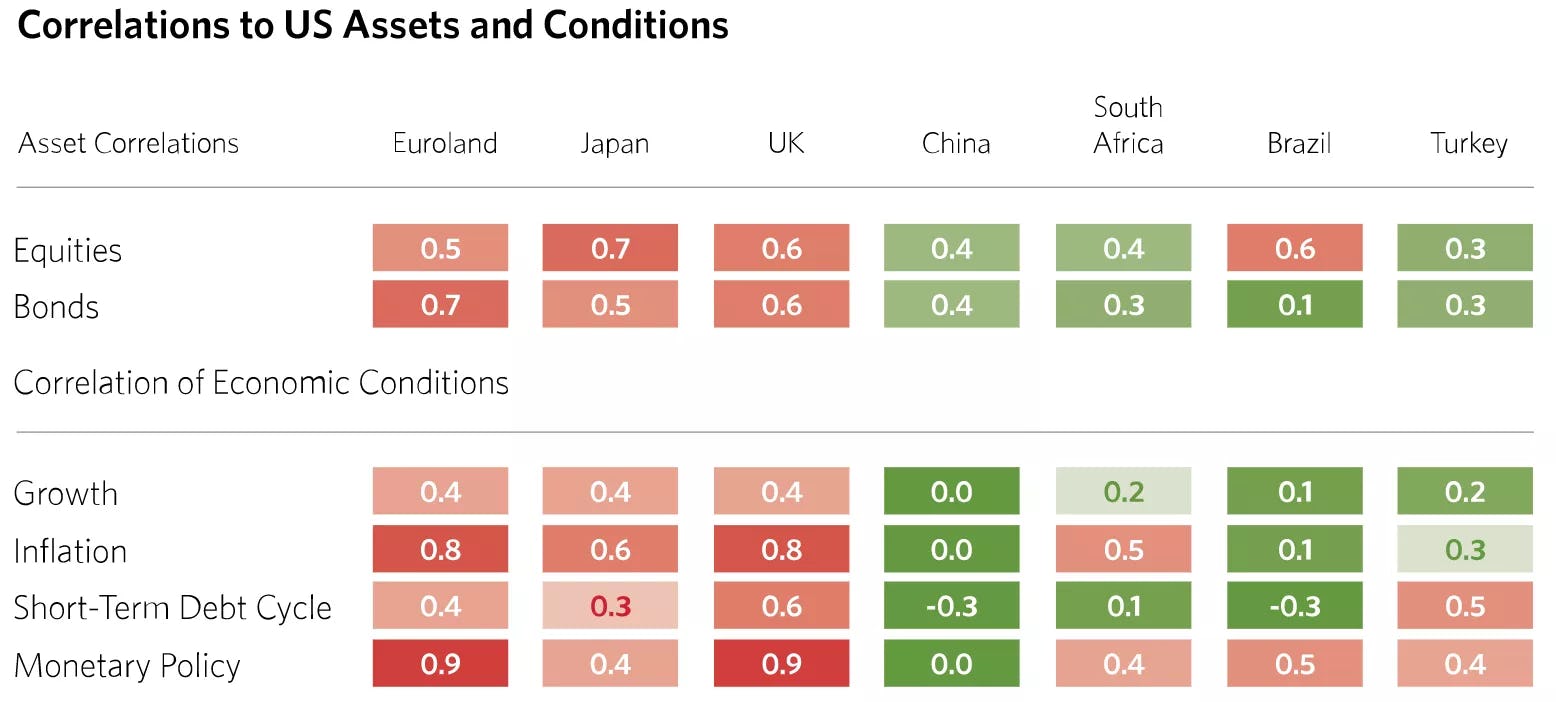

All of these forces raise the importance of diversification going forward. The table below reflects how lowly correlated the Chinese economy and its markets have been.”

Source: Bridgewater Associates titled ‘Geographic Diversification Can Be A Lifesaver – Yet Most Portfolios Are Highly Concentrated’, 2019.

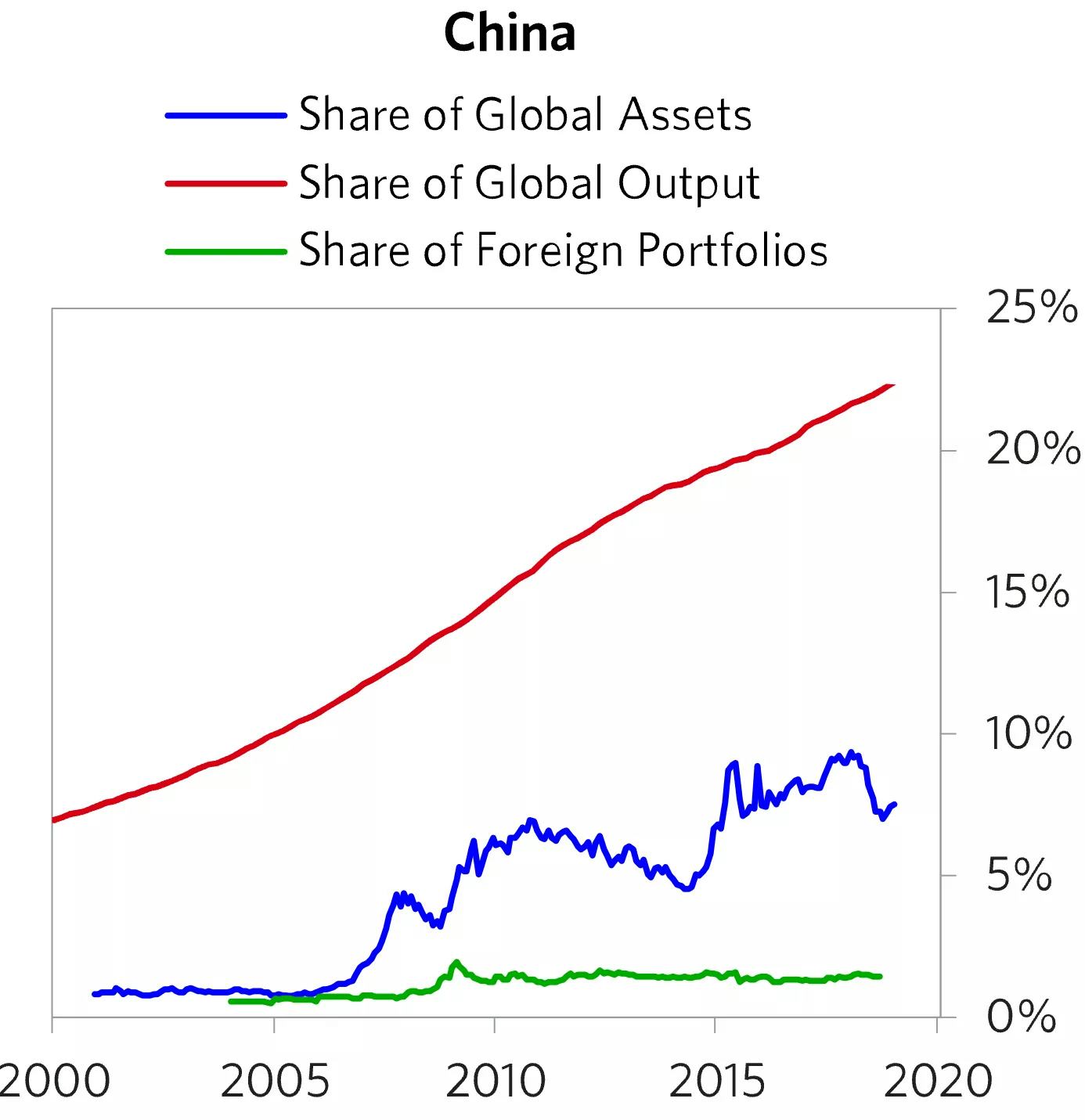

This recognition has surfaced at a time when China’s exposure in investors’ global portfolios is still small.

Bridgewater notes “Global portfolio exposure to China is tiny, though it is growing as Chinese markets gradually open up, making significant geographic diversification easier for investors to achieve.”

In 2020, Baillie Gifford made similar observations regarding the China market: “It’s under-owned. It counts for about 18% of the global market cap, 30% of listed stocks yet just 2.5% of global funds.”

Source: Bridgewater Associates titled ‘Geographic Diversification Can Be A Lifesaver – Yet Most Portfolios Are Highly Concentrated’, 2019.

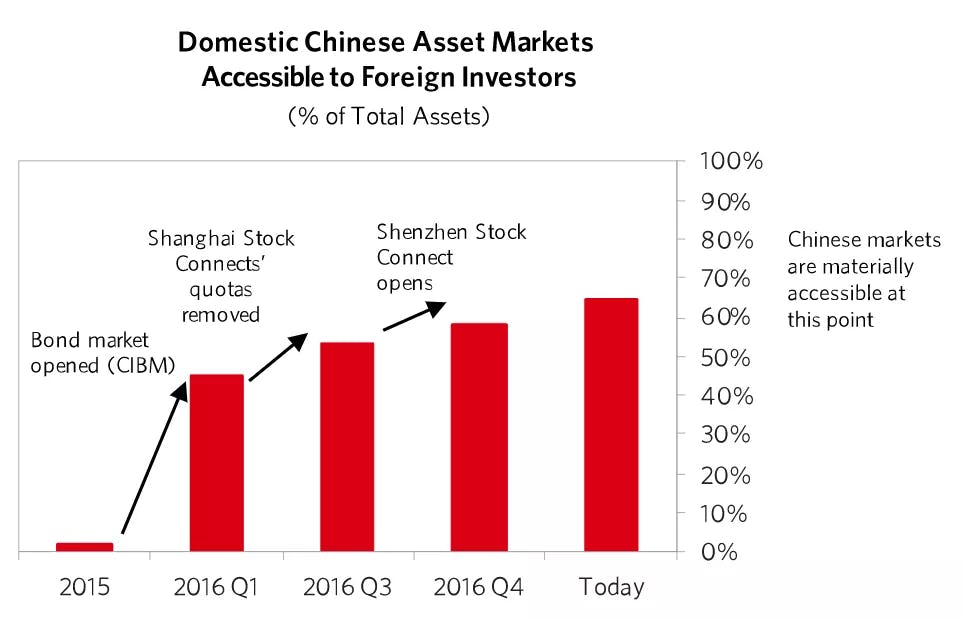

Research recommends China exposure

When investing, it’s always helpful to have a tailwind of demand. Tailwinds in China are likely to continue as it opens up its capital markets to global investors.

A Financial Times article from October 2020 titled, ‘China boosts foreign access to huge onshore capital markets,’ noted new rules making it easier for international investors to trade in China’s booming capital markets, improving investors’ ability to hedge positions, “one of the very important preconditions for people to scale up on their exposure in the market.”

In response to China’s welcoming of foreign capital, MSCI, FTSE Russell and the S&P Dow Jones have increased the weighting of China’s onshore shares in their indices.

Moreover, research from asset allocation advisory firm Willis Towers Watson says, “...investors have overlooked China and they should increase their average growth portfolio exposure of five per cent up to as much as 20 per cent over the next decade.”

Source: Bridgewater Associates titled ‘Geographic Diversification Can Be A Lifesaver – Yet Most Portfolios Are Highly Concentrated’, 2019.

China – worthy of a dedicated allocation

The size and scale of China’s equity market makes it worthy of a dedicated allocation, rather than simply a part of an emerging markets constituent.

Overlooking Chinese investment opportunities due to a home bias may result in foregoing exposure to many of the world’s largest and fastest growing corporations.

As always, the key for investors is taking the right approach. Particularly when investing offshore it may be wise to consider an active manager with a strong track-record and deep insights into the local landscape enabling a risk-managed approach to uncover the best opportunities.

>> For more information about our equities capabilities and solutions, please get in touch.

1. Represents average returns of major Chinese on-shore equities indices, including SSE Composite Index, China Shenzhen CSI 300, SZSE Composite Index and SZSE A-share Index.

2. calculated as % domestic equity over total equity exposure divided by the country weight in FTSE All-World Index.

Source: Bridgewater Associates titled ‘Geographic Diversification Can Be A Lifesaver – Yet Most Portfolios Are Highly Concentrated’, 2019. https://www.bridgewater.com/research-and-insights/geographic-diversification-can-be-a-lifesaver-yet-most-portfolios-are-highly-geographically-concentrated

Important Information: This material has been prepared by MA Investment Management Pty Ltd (ACN 621 552 896) (“MA Financial Group”), a Corporate Authorised Representative of MA Asset Management Ltd (ACN 142 008 535) (AFSL 327 515). The material is for general information purposes and must not be construed as investment advice. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer or invitation to purchase, sell or subscribe for in interests in any type of investment product or service. This material does not take into account your investment objectives, financial situation or particular needs. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. This material and the information contained within it may not be reproduced or disclosed, in whole or in part, without the prior written consent of MA Financial Group. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners.

Nothing contained herein should be construed as granting by implication, or otherwise, any licence or right to use any trademark displayed without the written permission of the owner. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of MA Financial Group. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Additionally, this material may contain “forward-looking statements”. Actual events or results or the actual performance of a MA Financial Group financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. Certain economic, market or company information contained herein has been obtained from published sources prepared by third parties. While such sources are believed to be reliable, neither MA Financial Group or any of its respective officers or employees assumes any responsibility for the accuracy or completeness of such information. No person, including MA Financial Group, has any responsibility to update any of the information provided in this material.